Hi,

I feel somewhat sorry for spamming these forums for help but here goes..

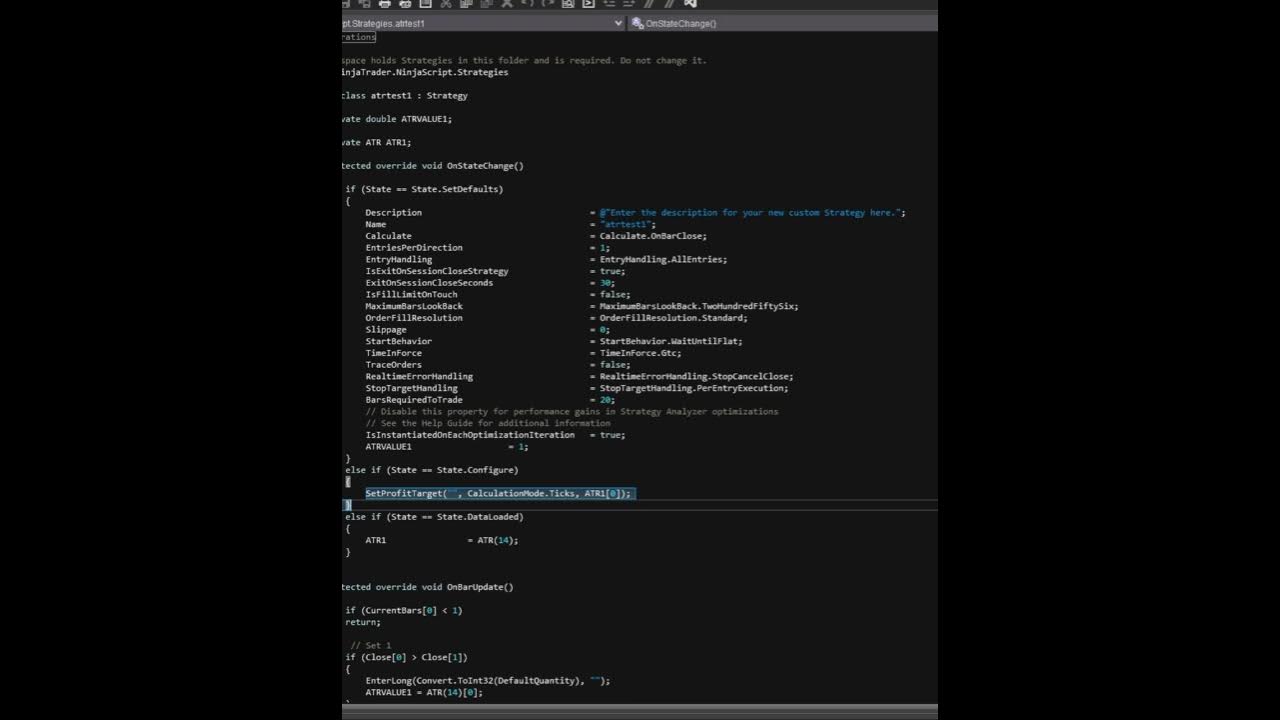

I tried to follow this video guide for NT7 for adding TP & SL from ATR:

I tried to "translate" the parameters and process to NT8 to no avail. Can this be done in NT8 through the Wizard?

Thanks again in advance!

br,

Chris

I feel somewhat sorry for spamming these forums for help but here goes..

I tried to follow this video guide for NT7 for adding TP & SL from ATR:

I tried to "translate" the parameters and process to NT8 to no avail. Can this be done in NT8 through the Wizard?

Thanks again in advance!

br,

Chris

Comment